Market developments

The date January 1, 2026 is rapidly approaching, and with it, the implementation of the CBAM measures. This means that from that date onwards, payment will be required for CO₂ emissions associated with imported steel materials from outside the EU. Due to circulating rumors about a possible delay, the European Commission reaffirmed at the end of August that there will be no postponement and that CBAM will indeed come into effect on January 1, 2026.

It is still unclear what the exact costs for imported CO₂ emissions will be, which must be paid once a certain threshold is exceeded. Expectations range between €50–100 per ton, but these vary widely and differ per product group. The European Commission is still working on the detailed implementation of the CBAM regulation. A previous proposal for simplification has already been adopted by the European Parliament. Since actual payment for CO₂ emissions imported in 2026 will only be required in 2027, it remains uncertain when importers will start including these costs into their pricing.

Meanwhile, there is more clarity regarding new Safeguard agreements, which aim to limit steel imports from outside the EU to protect the domestic industry. The current Safeguard quotas will expire in July 2026. After intense discussions, the European Commission has proposed significant measures on October 8. The two main outcomes are:

1. The free import quota will be reduced by nearly half, to align with the decreased demand for steel.

2. Import duties will be increased from 25% to 50%, in response to the 50% import duties imposed by the US on European steel.

This proposal still needs to be approved by the individual member states. There is also uncertainty about the date these measures will take effect. It is possible that this will be earlier than July 1, 2026, when the current regulation officially expires.

Despite the fact that no final decision has been made and the effective date remains uncertain, we expect that the announcement of these measures will have a price-driving effect. However, it is unclear when and to what extent this will occur.

Steel demand in Europe remains consistently low, and according to Eurofer, substantial growth is not expected until sometime in 2026. However, this forecast is uncertain and depends on many geopolitical factors. There are a few sectors where investments are increasing, such as in installations for carbon capture and storage (CCS), the construction of data centers, and the defense industry.

October 2025

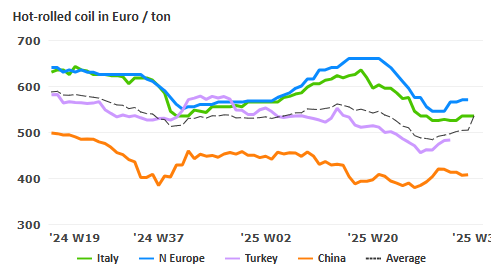

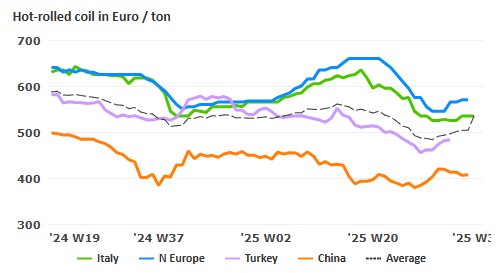

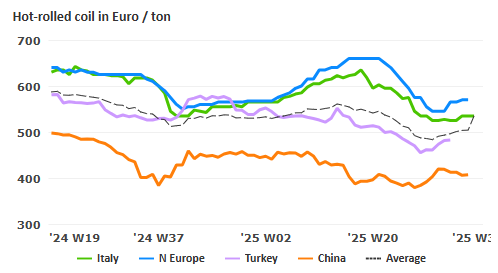

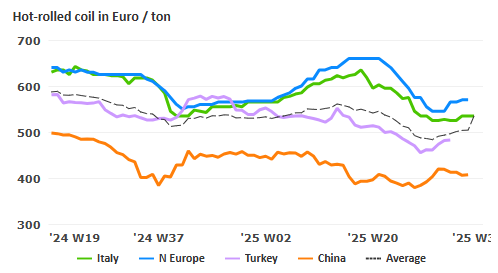

Price development of hot-rolled coil (source Kallanish)

Price development of scrap (source Kallanish)

Sustainability news

The recent commitment by the Dutch government to invest €2 billion in the sustainability of Tata Steel IJmuiden is welcome news. It acknowledges the importance of maintaining high-quality steel production in the Netherlands, while ensuring that this is done in a more sustainable and less polluting way.

We too continue to invest in sustainability, for example by developing a range of sustainably produced steel tubes under our brand Van Leeuwen Impact. Alongside other initiatives—such as using HVO100 biofuel for our customer deliveries and generating our own energy—we aim to become the world’s greenest tube distributor by 2030.

Availability and delivery times

The availability and lead times for tubes, fittings, and flanges have not changed significantly in the last quarter. We expect this to remain in line with market conditions in the coming months. Our stock levels are at the desired level.

Transport Cost

Due to an oversupply of container transport, prices have dropped sharply since September, especially on the Asia–Europe route.

However, the price level is still higher than in 2023.

Price developments of carbon steel products

Manufacturers of welded tubes have slightly increased their prices. It remains to be seen whether the market will accept these changes. Pressure is mounting, however, as producers of the base material (hot-rolled coil) are expected to incorporate CBAM-related costs into their pricing for the fourth quarter. This trend is already visible in price developments (see graph). And quite recently, the announced new Safeguard measures are adding further upward pressure on prices.

The price level for seamless tubes has remained unchanged since the summer. Rohrwerk Maxhütte, a manufacturer of seamless tubes, was declared bankrupt on September 1. On the other hand, another manufacturer, Interpipe, has announced that it will resume full production capacity from October/November after several months of repair work. Overall, this results in a stable market situation and stable pricing.

Manufacturers of fittings and flanges are being hit hard by U.S. import duties. Orders are either not coming in or are being accepted at significantly lower prices. Prices for base materials such as billet or plate remain stable, so we do not expect any notable changes in Europe in the short term.

Royal Van Leeuwen More than tubes.

Van Leeuwen Buizen Groep B.V.

Adres:

Telefoon:

E-mail:

Lindtsedijk 120, 3336 LE Zwijndrecht

078 625 25 25

vlptg@vanleeuwen.nl

Van Leeuwen

More than tubes.

Lindtsedijk 100, 3336 LE Zwijndrecht, Netherlands

+31 78 625 25 25

sales@vanleeuwen.nl

www.vanleeuwen.com

P. van Leeuwen Jr.'s Buizenhandel B.V.

Address:

Phone:

E-mail:

Web:

Never want to miss a Pipe and Tube Market Review and want to be the first to read it each quarter? Then follow us on LinkedIn!

© Royal Van Leeuwen 2025

The recent commitment by the Dutch government to invest €2 billion in the sustainability of Tata Steel IJmuiden is welcome news. It acknowledges the importance of maintaining high-quality steel production in the Netherlands, while ensuring that this is done in a more sustainable and less polluting way.

We too continue to invest in sustainability, for example by developing a range of sustainably produced steel tubes under our brand Van Leeuwen Impact. Alongside other initiatives—such as using HVO100 biofuel for our customer deliveries and generating our own energy—we aim to become the world’s greenest tube distributor by 2030.

Transport Cost

Due to an oversupply of container transport, prices have dropped sharply since September, especially on the Asia–Europe route.

However, the price level is still higher than in 2023.

Sustainability news

Last month, the European Commission took an important decision “to fund research for breakthrough technologies leading to near-zero-carbon steelmaking, as well as projects for managing the just transition for coal mines”. Read more about this program here: Research Program of the Research Fund for Coal and Steel (RFCS).

This program turns out to be part of a much bigger initiative from the EU which was announced on February 26: the “Clean Industrial Deal”. In this deal the Commission outlines three main objectives: ensure affordable energy, boost the demand for clean products and finance the clean transition. For this last objective, an “industrial decarbonisation bank” of 100 million Euro should be set up. Many companies want to invest in the clean energy transition, they often have very concrete plans, but fail to get the business case positive. This fund will therefore be a very important part to boost the energy transition,

Within these three objectives, more plans have been worked out. On of them is to improve efficiency and effectiveness of the existing CBAM regulation. This Carbon Border Adjustment Mechanism has been created to prevent carbon leakage at EU borders, which could occur by relocating carbon intensive production to less carbon-regulated countries. It should also stimulate more sustainable production methods within the EU.

Availability and delivery times

The availability and lead times for tubes, fittings, and flanges have not changed significantly in the last quarter. We expect this to remain in line with market conditions in the coming months. Our stock levels are at the desired level.

Price developments of carbon steel products

Manufacturers of welded tubes have slightly increased their prices. It remains to be seen whether the market will accept these changes. Pressure is mounting, however, as producers of the base material (hot-rolled coil) are expected to incorporate CBAM-related costs into their pricing for the fourth quarter. This trend is already visible in price developments (see graph). And quite recently, the announced new Safeguard measures are adding further upward pressure on prices.

The price level for seamless tubes has remained unchanged since the summer. Rohrwerk Maxhütte, a manufacturer of seamless tubes, was declared bankrupt on September 1. On the other hand, another manufacturer, Interpipe, has announced that it will resume full production capacity from October/November after several months of repair work. Overall, this results in a stable market situation and stable pricing.

Manufacturers of fittings and flanges are being hit hard by U.S. import duties. Orders are either not coming in or are being accepted at significantly lower prices. Prices for base materials such as billet or plate remain stable, so we do not expect any notable changes in Europe in the short term.

Price development of hot-rolled coil (source Kallanish)

Price development of scrap (source Kallanish)

Market developments

The date January 1, 2026 is rapidly approaching, and with it, the implementation of the CBAM measures. This means that from that date onwards, payment will be required for CO₂ emissions associated with imported steel materials from outside the EU. Due to circulating rumors about a possible delay, the European Commission reaffirmed at the end of August that there will be no postponement and that CBAM will indeed come into effect on January 1, 2026.

It is still unclear what the exact costs for imported CO₂ emissions will be, which must be paid once a certain threshold is exceeded. Expectations range between €50–100 per ton, but these vary widely and differ per product group. The European Commission is still working on the detailed implementation of the CBAM regulation. A previous proposal for simplification has already been adopted by the European Parliament. Since actual payment for CO₂ emissions imported in 2026 will only be required in 2027, it remains uncertain when importers will start including these costs into their pricing.

Meanwhile, there is more clarity regarding new Safeguard agreements, which aim to limit steel imports from outside the EU to protect the domestic industry. The current Safeguard quotas will expire in July 2026. After intense discussions, the European Commission has proposed significant measures on October 8. The two main outcomes are:

1. The free import quota will be reduced by nearly half, to align with the decreased demand for steel.

2. Import duties will be increased from 25% to 50%, in response to the 50% import duties imposed by the US on European steel.

This proposal still needs to be approved by the individual member states. There is also uncertainty about the date these measures will take effect. It is possible that this will be earlier than July 1, 2026, when the current regulation officially expires.

Despite the fact that no final decision has been made and the effective date remains uncertain, we expect that the announcement of these measures will have a price-driving effect. However, it is unclear when and to what extent this will occur.

Steel demand in Europe remains consistently low, and according to Eurofer, substantial growth is not expected until sometime in 2026. However, this forecast is uncertain and depends on many geopolitical factors. There are a few sectors where investments are increasing, such as in installations for carbon capture and storage (CCS), the construction of data centers, and the defense industry.

© Royal Van Leeuwen 2025

Royal Van Leeuwen More than tubes.

Lindtsedijk 120, 3336 LE Zwijndrecht

078 625 25 25

vlptg@vanleeuwen.nl

October 2025