Developments in the steel market

Outlook steel market

In 2025, contrary to earlier expectations of more favorable market conditions, the European steel consumption declined, also driven by tariffs and resulting uncertainty and trade related disruptions. In the last quarter of 2025, the European steel market shows early signs of stabilization and the European steel consumption is projected to recover in 2026. There are a few industries where investments are increasing, such as in installations for carbon capture and storage (CCS), the construction and defense industry. The overall developments of the steel market remain subject to very high uncertainty and the outlook for the first quarter 2026 remains cautious.

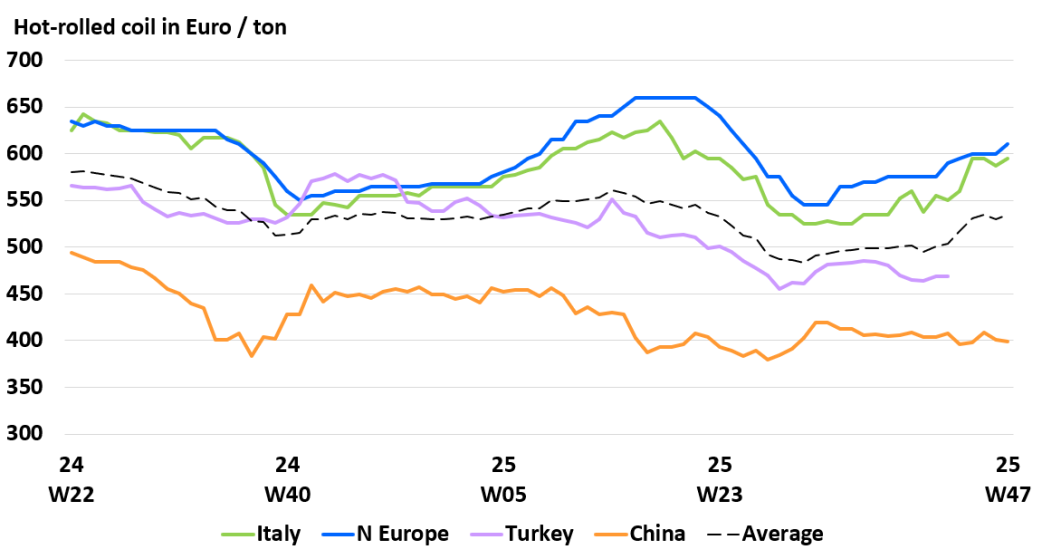

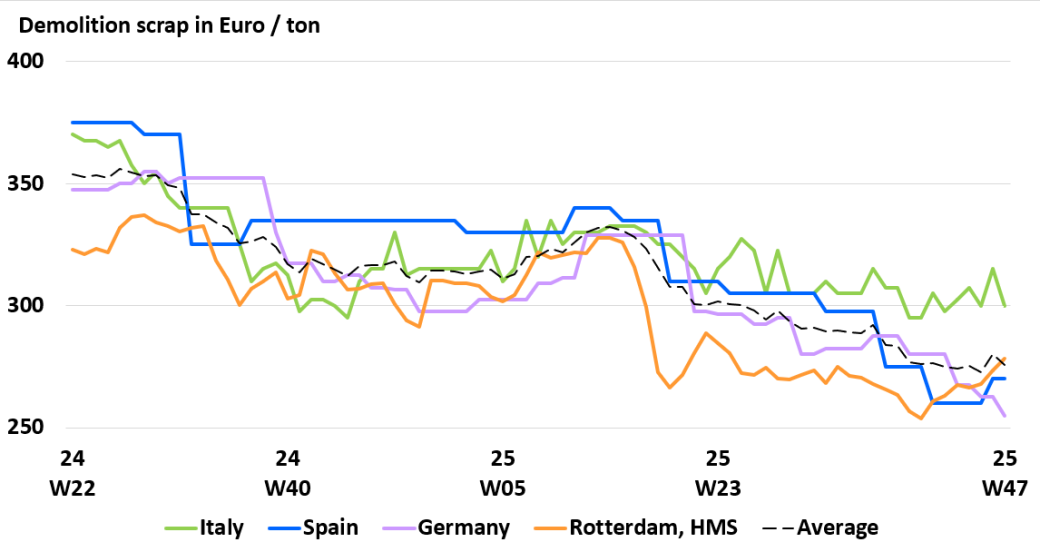

The introduction of CBAM from January 1st, 2026 and the planned safeguard measures are still influencing the market and many buyers are preparing for the upcoming changes. In October, a strong pre-CBAM stocking was done with a record-high import activity. Buying behavior has shifted towards shorter delivery periods and companies are delaying large orders until there is more clarity about the upcoming requirements. The inventories in the steel market remain low across much of the supply chain. This could potentially lead to a tighter availability once the demand picks up again. Manufacturers of welded pipes & tubes have increased their prices, based on rising pre-material prices. Producers of hot-rolled coils are incorporating CBAM-related costs into their pricing, buyers shifting from imports to domestic suppliers.

The announced new EU-Safeguard measures are adding further upward pressure on prices. The price level for seamless tubes has remained unchanged in the last weeks. The German seamless pipe & tube producer Rohrwerk Maxhütte declared bankruptcy on September 1. On the other hand, another manufacturer, Interpipe, has announced that it will resume full production capacity from November after several months of repair work. Overall, this results in a stable market situation until year-end. The availability and lead times for steel pipes & tubes, fittings, and flanges have not changed significantly in the last weeks. We expect this to remain in line with market conditions in the coming months. Our stock levels ensures customer-oriented delivery.

The introduction of CBAM from January 1st, 2026 and the planned safeguard measures are still influencing the market and many buyers are preparing for the upcoming changes. In October, a strong pre-CBAM stocking was done with a record-high import activity. Buying behavior has shifted towards shorter delivery periods and companies are delaying large orders until there is more clarity about the upcoming requirements. The inventories in the steel market remain low across much of the supply chain. This could potentially lead to a tighter availability once the demand picks up again. Manufacturers of welded pipes & tubes have increased their prices, based on rising pre-material prices. Producers of hot-rolled coils are incorporating CBAM-related costs into their pricing, buyers shifting from imports to domestic suppliers.

The announced new EU-Safeguard measures are adding further upward pressure on prices. The price level for seamless tubes has remained unchanged in the last weeks. The German seamless pipe & tube producer Rohrwerk Maxhütte declared bankruptcy on September 1. On the other hand, another manufacturer, Interpipe, has announced that it will resume full production capacity from November after several months of repair work. Overall, this results in a stable market situation until year-end. The availability and lead times for steel pipes & tubes, fittings, and flanges have not changed significantly in the last weeks. We expect this to remain in line with market conditions in the coming months. Our stock levels ensures customer-oriented delivery.

Update CBAM and safeguard measures

The European steel market is preparing for two major regulatory developments: the full introduction of CBAM and the upcoming adjustments to the EU safeguard measures. Both will shape pricing, availability and import dynamics in 2026.

From January 1, 2026, the Carbon Border Adjustment Mechanism (CBAM) will apply to reduce the Co₂-emissions of imported steel products. While the exact certificate price will be confirmed later, expectations range between €50-€150 per ton. This means that carbon-related costs will already influence import prices from early 2026 onward.

Additionally, the European Commission has made a proposal on the new safeguard measures that limit annual steel import volumes. A significant reduction of 1.8 million tons is implemented, which is 57% less imports. Also, for HRC a reduction of 4.3 million tons is foreseen. Lastly, the proposal states an increase on the over-quota tariff from 25% to 50%. These measures are expected to increase the price pressure and temporarily affect product availability.

With our global network and strong supplier base, Van Leeuwen is well positioned to navigate these changes and continue supporting our customers with reliable supply and clear guidance.

The European steel market is preparing for two major regulatory developments: the full introduction of CBAM and the upcoming adjustments to the EU safeguard measures. Both will shape pricing, availability and import dynamics in 2026.

From January 1, 2026, the Carbon Border Adjustment Mechanism (CBAM) will apply to reduce the Co₂-emissions of imported steel products. While the exact certificate price will be confirmed later, expectations range between €50-€150 per ton. This means that carbon-related costs will already influence import prices from early 2026 onward.

Additionally, the European Commission has made a proposal on the new safeguard measures that limit annual steel import volumes. A significant reduction of 1.8 million tons is implemented, which is 57% less imports. Also, for HRC a reduction of 4.3 million tons is foreseen. Lastly, the proposal states an increase on the over-quota tariff from 25% to 50%. These measures are expected to increase the price pressure and temporarily affect product availability.

With our global network and strong supplier base, Van Leeuwen is well positioned to navigate these changes and continue supporting our customers with reliable supply and clear guidance.

Tariffs, safeguard and CBAM

In response to unfair trade practices as well as global overcapacity, the European Commission will introduce new long-term steel safeguards. The Commission announced its Steel and Metals Action Plan in March, aimed at securing competitiveness, and decarbonization of Europe’s steel and metals industries. This includes more protection against dumping and a better functioning of the CO2-regulation. To prevent carbon leakage, the Commission will strengthen CBAM with anti-circumvention measures and extend its scope to downstream steel and aluminium products.

Important news for the steel market is that the United States imposed tariffs of up to 50% on imports of steel, aluminium, and certain products containing steel and aluminium from the European Union. Although the consequences are difficult to predict, this is expected have an impact on global material flows and price levels.e-impact-on-the-market-for-steel-tube-products/

In response to unfair trade practices as well as global overcapacity, the European Commission will introduce new long-term steel safeguards. The Commission announced its Steel and Metals Action Plan in March, aimed at securing competitiveness, and decarbonization of Europe’s steel and metals industries. This includes more protection against dumping and a better functioning of the CO2-regulation. To prevent carbon leakage, the Commission will strengthen CBAM with anti-circumvention measures and extend its scope to downstream steel and aluminium products.

Important news for the steel market is that the United States imposed tariffs of up to 50% on imports of steel, aluminium, and certain products containing steel and aluminium from the European Union. Although the consequences are difficult to predict, this is expected have an impact on global material flows and price levels.e-impact-on-the-market-for-steel-tube-products/

In 2025, contrary to earlier expectations of more favorable market conditions, the European steel consumption declined, also driven by tariffs and resulting uncertainty and trade related disruptions. In the last quarter of 2025, the European steel market shows early signs of stabilization and the European steel consumption is projected to recover in 2026. There are a few industries where investments are increasing, such as in installations for carbon capture and storage (CCS), the construction and defense industry. The overall developments of the steel market remain subject to very high uncertainty and the outlook for the first quarter 2026 remains cautious.

The introduction of CBAM from January 1st, 2026 and the planned safeguard measures are still influencing the market and many buyers are preparing for the upcoming changes. In October, a strong pre-CBAM stocking was done with a record-high import activity. Buying behavior has shifted towards shorter delivery periods and companies are delaying large orders until there is more clarity about the upcoming requirements. The inventories in the steel market remain low across much of the supply chain. This could potentially lead to a tighter availability once the demand picks up again. Manufacturers of welded pipes & tubes have increased their prices, based on rising pre-material prices. Producers of hot-rolled coils are incorporating CBAM-related costs into their pricing, buyers shifting from imports to domestic suppliers.

The announced new EU-Safeguard measures are adding further upward pressure on prices. The price level for seamless tubes has remained unchanged in the last weeks. The German seamless pipe & tube producer Rohrwerk Maxhütte declared bankruptcy on September 1. On the other hand, another manufacturer, Interpipe, has announced that it will resume full production capacity from November after several months of repair work. Overall, this results in a stable market situation until year-end. The availability and lead times for steel pipes & tubes, fittings, and flanges have not changed significantly in the last weeks. We expect this to remain in line with market conditions in the coming months. Our stock levels ensures customer-oriented delivery.

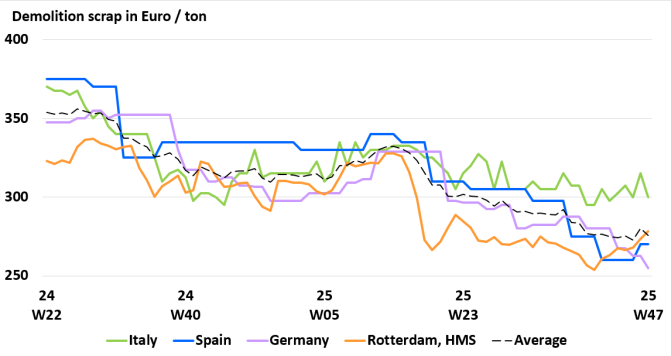

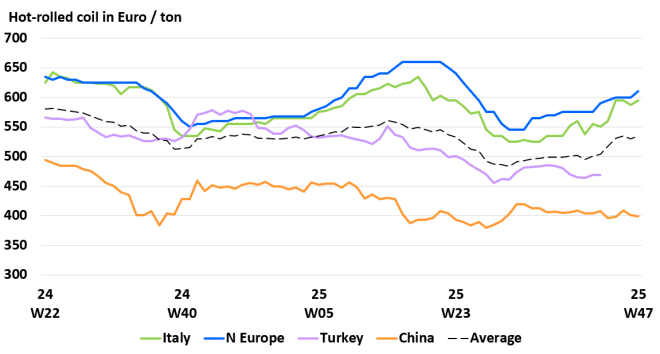

The introduction of CBAM from January 1st, 2026 and the planned safeguard measures are still influencing the market and many buyers are preparing for the upcoming changes. In October, a strong pre-CBAM stocking was done with a record-high import activity. Buying behavior has shifted towards shorter delivery periods and companies are delaying large orders until there is more clarity about the upcoming requirements. The inventories in the steel market remain low across much of the supply chain. This could potentially lead to a tighter availability once the demand picks up again. Manufacturers of welded pipes & tubes have increased their prices, based on rising pre-material prices. Producers of hot-rolled coils are incorporating CBAM-related costs into their pricing, buyers shifting from imports to domestic suppliers.

The announced new EU-Safeguard measures are adding further upward pressure on prices. The price level for seamless tubes has remained unchanged in the last weeks. The German seamless pipe & tube producer Rohrwerk Maxhütte declared bankruptcy on September 1. On the other hand, another manufacturer, Interpipe, has announced that it will resume full production capacity from November after several months of repair work. Overall, this results in a stable market situation until year-end. The availability and lead times for steel pipes & tubes, fittings, and flanges have not changed significantly in the last weeks. We expect this to remain in line with market conditions in the coming months. Our stock levels ensures customer-oriented delivery.

Outlook steel market

Developments in the steel market