Developments in the steel market

Outlook steel market

For the first half of 2026, the European economy shows some signs of recovery. Industrial sentiment is improving and modest growth is expected. However, the outlook still remains sensitive to geopolitical developments. Additionally, the energy price volatility plays a key role.

Steel demand is expected to slightly increase in 2026. This is supported by the gradual recovery in key steel-consuming sectors. The outlook however differs per segment. Mechanical engineering and parts of the construction sector show early signs of improvement, while the automotive industry still faces challenges. This is due to weaker export performance and cautious investment behavior. Overall, the demand is stable but not yet at a strong level.

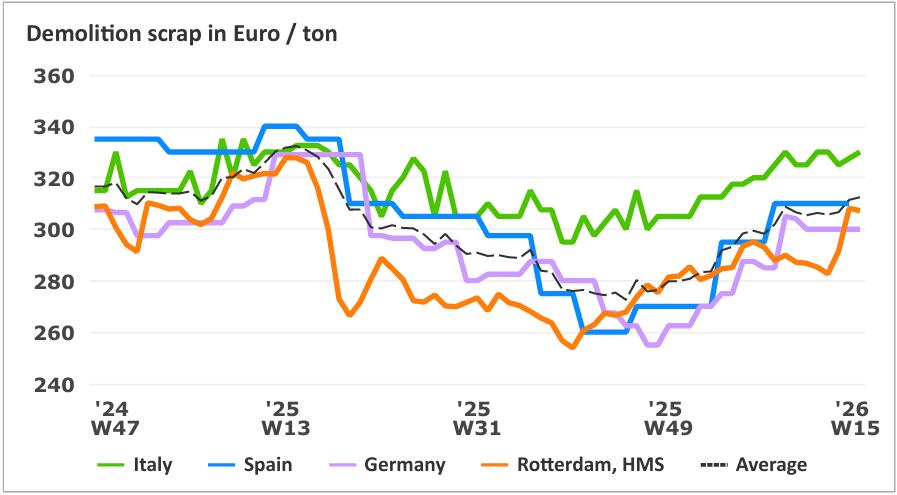

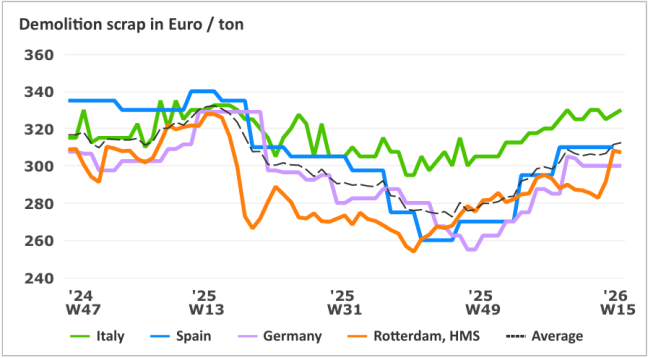

The raw material development is in line with the current market situation. Iron ore prices have stayed relatively stable. But scrap prices show moderate increases depending on region. At the same time, energy costs have become more volatile again due to geopolitical developments. This directly impacts production costs for European mills.

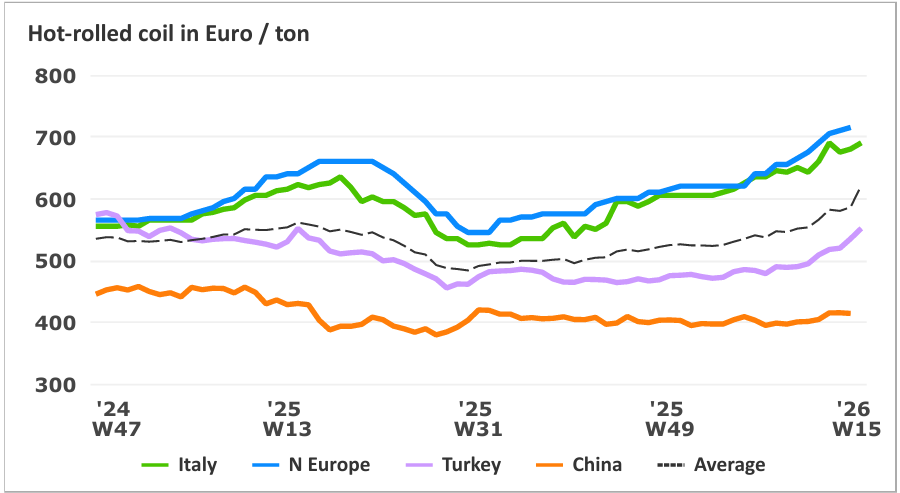

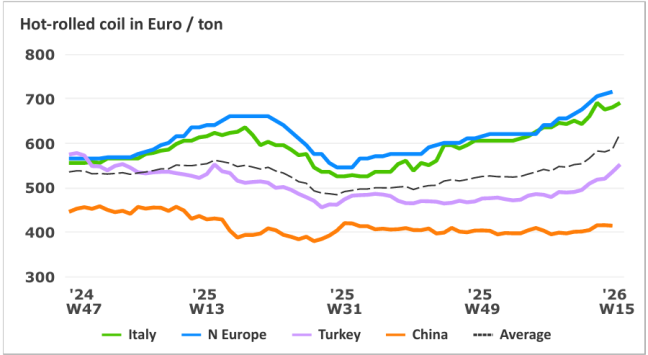

Price levels for hot rolled coil have increased further since the start of the year. This is supported by the reduced import volumes and tighter availability in the European market. Current levels are around €690-710/t, with expectations of a gradual increase towards €760–780/t in the coming months.

Delivery times for most steel products are gradually increasing, showing the tighter supply conditions. The availability of imports stays limited, while European mills maintain disciplined production levels. Price developments in the coming months will depend on import flows and the development of energy costs.

Steel demand is expected to slightly increase in 2026. This is supported by the gradual recovery in key steel-consuming sectors. The outlook however differs per segment. Mechanical engineering and parts of the construction sector show early signs of improvement, while the automotive industry still faces challenges. This is due to weaker export performance and cautious investment behavior. Overall, the demand is stable but not yet at a strong level.

The raw material development is in line with the current market situation. Iron ore prices have stayed relatively stable. But scrap prices show moderate increases depending on region. At the same time, energy costs have become more volatile again due to geopolitical developments. This directly impacts production costs for European mills.

Price levels for hot rolled coil have increased further since the start of the year. This is supported by the reduced import volumes and tighter availability in the European market. Current levels are around €690-710/t, with expectations of a gradual increase towards €760–780/t in the coming months.

Delivery times for most steel products are gradually increasing, showing the tighter supply conditions. The availability of imports stays limited, while European mills maintain disciplined production levels. Price developments in the coming months will depend on import flows and the development of energy costs.

The impact of CBAM and the upcoming Safeguard revision is becoming more and more visible in the European steel market.

CBAM is already affecting pricing dynamics, with initial calculations indicating that the cost impact on imports can be higher than previously anticipated. At the same time, there remains uncertainty around the accreditation of actual emission values, with no clear timeline yet. This continues to support cautious buying behavior and a preference for shorter-term commitments.

Regarding Safeguard Measures, further clarity is expected only shortly before the expiry date of the current measures at the end of June. However, the anticipated changes are already influencing the market. A reduction in imports of around 42% year-on-year in Q3 2026 is being considered. To compensate for this, EU steel production would need to increase by approximately 20%. But this seems unlikely at this stage. Steelmakers are therefore expected to take a wait-and-see approach before committing to additional capacity.

If supply does not adjust in time, this could lead to temporary shortages. Additionally, the developments in the Middle East may further impact the competitiveness of Asian imports through rising freight costs and potential energy constraints.

CBAM is already affecting pricing dynamics, with initial calculations indicating that the cost impact on imports can be higher than previously anticipated. At the same time, there remains uncertainty around the accreditation of actual emission values, with no clear timeline yet. This continues to support cautious buying behavior and a preference for shorter-term commitments.

Regarding Safeguard Measures, further clarity is expected only shortly before the expiry date of the current measures at the end of June. However, the anticipated changes are already influencing the market. A reduction in imports of around 42% year-on-year in Q3 2026 is being considered. To compensate for this, EU steel production would need to increase by approximately 20%. But this seems unlikely at this stage. Steelmakers are therefore expected to take a wait-and-see approach before committing to additional capacity.

If supply does not adjust in time, this could lead to temporary shortages. Additionally, the developments in the Middle East may further impact the competitiveness of Asian imports through rising freight costs and potential energy constraints.

Update Carbon Border Adjustment Mechanism (CBAM) and Safeguard Measures

Update Carbon Border Adjustment Mechanism (CBAM) and Safeguard Measures

The impact of CBAM and the upcoming Safeguard revision is becoming more and more visible in the European steel market.

CBAM is already affecting pricing dynamics, with initial calculations indicating that the cost impact on imports can be higher than previously anticipated. At the same time, there remains uncertainty around the accreditation of actual emission values, with no clear timeline yet. This continues to support cautious buying behavior and a preference for shorter-term commitments.

Regarding Safeguard Measures, further clarity is expected only shortly before the expiry date of the current measures at the end of June. However, the anticipated changes are already influencing the market. A reduction in imports of around 42% year-on-year in Q3 2026 is being considered. To compensate for this, EU steel production would need to increase by approximately 20%. But this seems unlikely at this stage. Steelmakers are therefore expected to take a wait-and-see approach before committing to additional capacity.

If supply does not adjust in time, this could lead to temporary shortages. Additionally, the developments in the Middle East may further impact the competitiveness of Asian imports through rising freight costs and potential energy constraints.

CBAM is already affecting pricing dynamics, with initial calculations indicating that the cost impact on imports can be higher than previously anticipated. At the same time, there remains uncertainty around the accreditation of actual emission values, with no clear timeline yet. This continues to support cautious buying behavior and a preference for shorter-term commitments.

Regarding Safeguard Measures, further clarity is expected only shortly before the expiry date of the current measures at the end of June. However, the anticipated changes are already influencing the market. A reduction in imports of around 42% year-on-year in Q3 2026 is being considered. To compensate for this, EU steel production would need to increase by approximately 20%. But this seems unlikely at this stage. Steelmakers are therefore expected to take a wait-and-see approach before committing to additional capacity.

If supply does not adjust in time, this could lead to temporary shortages. Additionally, the developments in the Middle East may further impact the competitiveness of Asian imports through rising freight costs and potential energy constraints.

For the first half of 2026, the European economy shows some signs of recovery. Industrial sentiment is improving and modest growth is expected. However, the outlook still remains sensitive to geopolitical developments. Additionally, the energy price volatility plays a key role.

Steel demand is expected to slightly increase in 2026. This is supported by the gradual recovery in key steel-consuming sectors. The outlook however differs per segment. Mechanical engineering and parts of the construction sector show early signs of improvement, while the automotive industry still faces challenges. This is due to weaker export performance and cautious investment behavior. Overall, the demand is stable but not yet at a strong level.

The raw material development is in line with the current market situation. Iron ore prices have stayed relatively stable. But scrap prices show moderate increases depending on region. At the same time, energy costs have become more volatile again due to geopolitical developments. This directly impacts production costs for European mills.

Price levels for hot rolled coil have increased further since the start of the year. This is supported by the reduced import volumes and tighter availability in the European market. Current levels are around €690-710/t, with expectations of a gradual increase towards €760–780/t in the coming months.

Delivery times for most steel products are gradually increasing, showing the tighter supply conditions. The availability of imports stays limited, while European mills maintain disciplined production levels. Price developments in the coming months will depend on import flows and the development of energy costs.

Steel demand is expected to slightly increase in 2026. This is supported by the gradual recovery in key steel-consuming sectors. The outlook however differs per segment. Mechanical engineering and parts of the construction sector show early signs of improvement, while the automotive industry still faces challenges. This is due to weaker export performance and cautious investment behavior. Overall, the demand is stable but not yet at a strong level.

The raw material development is in line with the current market situation. Iron ore prices have stayed relatively stable. But scrap prices show moderate increases depending on region. At the same time, energy costs have become more volatile again due to geopolitical developments. This directly impacts production costs for European mills.

Price levels for hot rolled coil have increased further since the start of the year. This is supported by the reduced import volumes and tighter availability in the European market. Current levels are around €690-710/t, with expectations of a gradual increase towards €760–780/t in the coming months.

Delivery times for most steel products are gradually increasing, showing the tighter supply conditions. The availability of imports stays limited, while European mills maintain disciplined production levels. Price developments in the coming months will depend on import flows and the development of energy costs.

Outlook steel market

Developments in the steel market