Market developments

We are approaching the much anticipated date of July 1 quickly now; the date on which the new import restrictions of the EU will come into effect. These measures will go under the name “TRQ”: Tariff Rate Quota. Although the general outline has already been approved by the EC and the rates of 47% (import quota restrictions) and 50% (over-quota tariff) have been announced, we are still awaiting the definitive country allocations and other details, such as rules for countries with which the EU has made a special trade agreement. These uncertainties, so close to the start date of TRQ, have caused a freeze in purchase activities in the last few months. With demand being moderate, steel mills are pushing to maintain price levels and secure orders.

However, a few factors play a role in the expected upward steel price pressure after the summer holidays:

With TRQ in place, including the uncertainties, importing steel from outside the EU will be unattractive and risky. Therefore, EU mills expect - and already see - more demand from customers formerly sourcing outside the EU.

Steel producers margins are at an ultimate low, which is not stimulating steel mills to start up idle production facilities and increase supply.

Buyers are not building stocks ahead of TRQ tightening, so stocks in the supply chain are decreasing. This means buyers will be forced to accept higher prices when they need to fill stocks later this year.

The above mentioned special agreements of the EU with certain countries also concerns Ukraine. Long time it was expected Ukraine would get a "free pass" for both TRQ and CBAM, but this seems to have changed recently. We have to prepare for Ukraine being fully included in these regulations, which means an export quota of less than a third of the volume they normally export to the EU. This will affect two major steel pipe mills in Ukraine.

June 2026

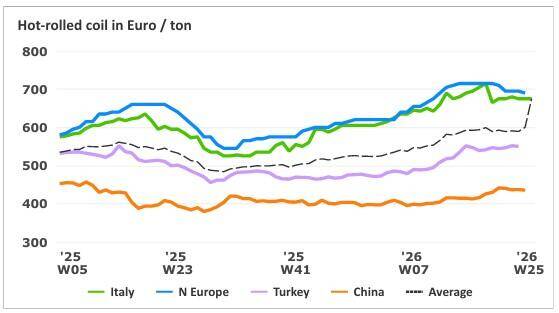

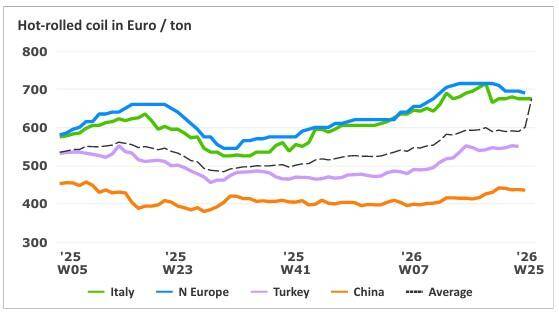

Price development of hot-rolled coil

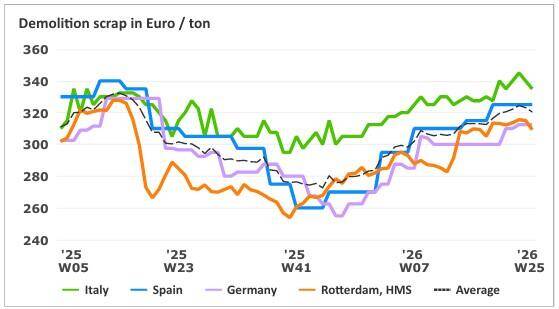

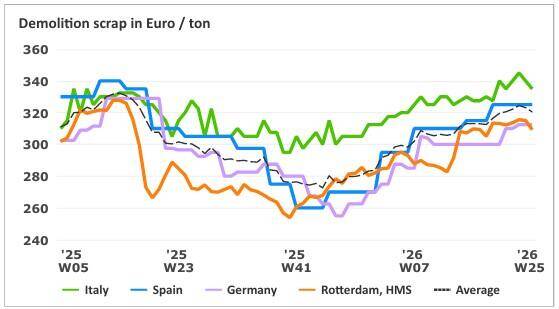

Price development of scrap

Sustainability news

Discussions about including steel products further down the supply chain in CBAM legislation are ongoing. As for now, only steel makers (the mills) are included in CBAM, and not the fabricators and manufacturers of steel based products further down the line. These are usually smaller companies, lacking a strong lobby organization as Eurofer is for the steel makers. If these companies are not protected by CBAM, they will face strong and unfair competition from outside the EU. These companies not only provide jobs, they are also important for the European industrial independence.

Availability and delivery times

Due to the modest market demand, delivery times are still normal and availability of steel tubes, fittings and flanges is good. We might see a change after the summer holidays, when TRQ will be effective and EU mills face a rising demand, especially from customers formerly buying outside the EU. Together with the limited production capacity, this might very well lead to orderbooks filling up quickly, making it possible for tube makers to impose their - much needed - price increases. This effect will be enhanced by the CBAM measures, which also make imports from outside the EU far less attractive and risky. CBAM tariffs are still unclear but will be implemented retroactively from 01.01.2026.

Transport Cost

In Europe, the war in the Middle East caused significant price increases for oil, gasoline and other fuels. This has lead to price increases for freight, both for truck and sea transport. Especially in May and June, strong price increases for sea container freight on the Europe – Asia route were noted. These higher energy cost are meanwhile filtering through into the steel tube distribution market.

Price developments of carbon steel products

Welded tubes

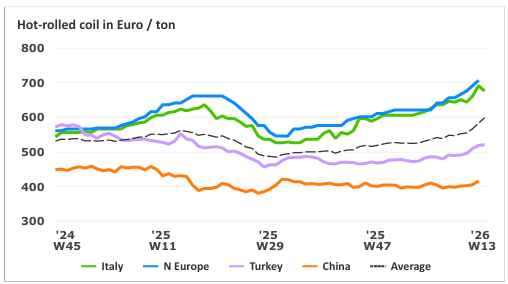

Purchase activities have been very low in the last months. Stockholders are consuming their stocks and delay refilling them, waiting for the details of TRQ and country allocations. Despite some upward price movement of HRC (see graph), prices for tubes have remained largely unchanged, due to the modest demand. However, we expect to see price increases in the second half of 2026. With TRQ are in place, imports will be highly unattractive and at the same time stockholders will have to build up their stocks.

Seamless tubes

The mills are sufficiently occupied and prices have remained stable. There are some changes on the supplier side. A tube mill in Spain was declared insolvent, but has resumed production and even accepts new orders while the insolvency administration is looking for possible solutions. Another seamless tube mill, in Romania, will probably be taken over. Both developments have not affected the market very much yet, beside some volume shifts. The biggest impact in this market could come from Ukraine. Two seamless tube mills will face a significant reduction of their quota when the EU decides that Ukraine will not get a fundamental exception from the TRQ measurements. This will cause an upward price pressure.

Fittings and Flanges

Producers of fittings and flanges are trying to raise their prices due to the increased price levels of raw materials (billets), energy and transport, but the lack of demand is making that very hard. For the coming months, with the summer break approaching, not much change is expected.

Royal Van Leeuwen More than tubes.

Van Leeuwen Buizen Groep B.V.

Adres:

Telefoon:

E-mail:

Lindtsedijk 120, 3336 LE Zwijndrecht

078 625 25 25

vlptg@vanleeuwen.nl

Van Leeuwen

More than tubes.

Lindtsedijk 100, 3336 LE Zwijndrecht, Netherlands

+31 78 625 25 25

sales@vanleeuwen.nl

www.vanleeuwen.com

P. van Leeuwen Jr.'s Buizenhandel B.V.

Address:

Phone:

E-mail:

Web:

Never want to miss a Pipe and Tube Market Review and want to be the first to read it each quarter? Then follow us on LinkedIn!

© Royal Van Leeuwen 2026

Discussions about including steel products further down the supply chain in CBAM legislation are ongoing. As for now, only steel makers (the mills) are included in CBAM, and not the fabricators and manufacturers of steel based products further down the line. These are usually smaller companies, lacking a strong lobby organization as Eurofer is for the steel makers. If these companies are not protected by CBAM, they will face strong and unfair competition from outside the EU. These companies not only provide jobs, they are also important for the European industrial independence.

Transport Cost

In Europe, the war in the Middle East caused significant price increases for oil, gasoline and other fuels. This has lead to price increases for freight, both for truck and sea transport. Especially in May and June, strong price increases for sea container freight on the Europe – Asia route were noted. These higher energy cost are meanwhile filtering through into the steel tube distribution market.

Sustainability news

Availability and delivery times

Due to the modest market demand, delivery times are still normal and availability of steel tubes, fittings and flanges is good. We might see a change after the summer holidays, when TRQ will be effective and EU mills face a rising demand, especially from customers formerly buying outside the EU. Together with the limited production capacity, this might very well lead to orderbooks filling up quickly, making it possible for tube makers to impose their - much needed - price increases. This effect will be enhanced by the CBAM measures, which also make imports from outside the EU far less attractive and risky. CBAM tariffs are still unclear but will be implemented retroactively from 01.01.2026.

Price developments of carbon steel products

Welded tubes

Purchase activities have been very low in the last months. Stockholders are consuming their stocks and delay refilling them, waiting for the details of TRQ and country allocations. Despite some upward price movement of HRC (see graph), prices for tubes have remained largely unchanged, due to the modest demand. However, we expect to see price increases in the second half of 2026. With TRQ are in place, imports will be highly unattractive and at the same time stockholders will have to build up their stocks.

Seamless tubes

The mills are sufficiently occupied and prices have remained stable. There are some changes on the supplier side. A tube mill in Spain was declared insolvent, but has resumed production and even accepts new orders while the insolvency administration is looking for possible solutions. Another seamless tube mill, in Romania, will probably be taken over. Both developments have not affected the market very much yet, beside some volume shifts. The biggest impact in this market could come from Ukraine. Two seamless tube mills will face a significant reduction of their quota when the EU decides that Ukraine will not get a fundamental exception from the TRQ measurements. This will cause an upward price pressure.

Fittings and Flanges

Producers of fittings and flanges are trying to raise their prices due to the increased price levels of raw materials (billets), energy and transport, but the lack of demand is making that very hard. For the coming months, with the summer break approaching, not much change is expected.

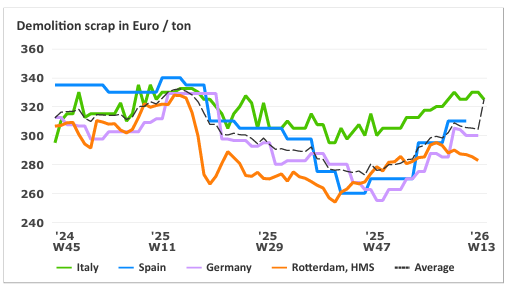

Price development of hot-rolled coil

Price development of scrap

Market developments

We are approaching the much anticipated date of July 1 quickly now; the date on which the new import restrictions of the EU will come into effect. These measures will go under the name “TRQ”: Tariff Rate Quota. Although the general outline has already been approved by the EC and the rates of 47% (import quota restrictions) and 50% (over-quota tariff) have been announced, we are still awaiting the definitive country allocations and other details, such as rules for countries with which the EU has made a special trade agreement. These uncertainties, so close to the start date of TRQ, have caused a freeze in purchase activities in the last few months. With demand being moderate, steel mills are pushing to maintain price levels and secure orders.

However, a few factors play a role in the expected upward steel price pressure after the summer holidays:

With TRQ in place, including the uncertainties, importing steel from outside the EU will be unattractive and risky. Therefore, EU mills expect - and already see - more demand from customers formerly sourcing outside the EU.

Steel producers margins are at an ultimate low, which is not stimulating steel mills to start up idle production facilities and increase supply.

Buyers are not building stocks ahead of TRQ tightening, so stocks in the supply chain are decreasing. This means buyers will be forced to accept higher prices when they need to fill stocks later this year.

The above mentioned special agreements of the EU with certain countries also concerns Ukraine. Long time it was expected Ukraine would get a "free pass" for both TRQ and CBAM, but this seems to have changed recently. We have to prepare for Ukraine being fully included in these regulations, which means an export quota of less than a third of the volume they normally export to the EU. This will affect two major steel pipe mills in Ukraine.

© Royal Van Leeuwen 2026

Royal Van Leeuwen More than tubes.

Lindtsedijk 120, 3336 LE Zwijndrecht

078 625 25 25

vlptg@vanleeuwen.nl

June 2026